What is Select Risk Captive (SRC)?

Select Risk Captive (SRC) is a member-owned captive insurance program created exclusively for established cannabis operators. It is designed to replace traditional guaranteed-cost insurance with a structure that delivers broader coverage, transparent claims handling, and long-term capital retention—while remaining fully compliant with regulatory requirements.

How is SRC different from traditional cannabis insurance?

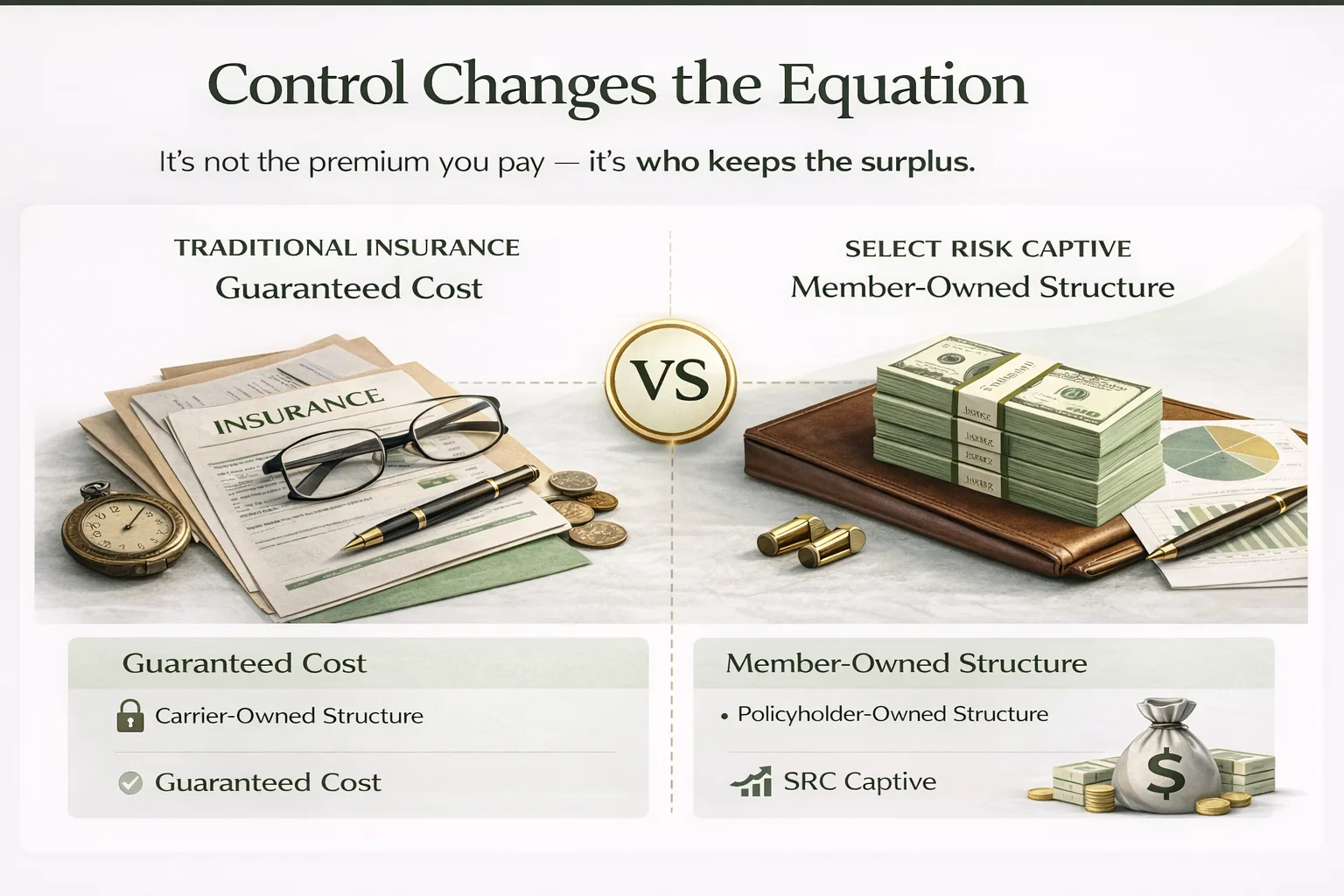

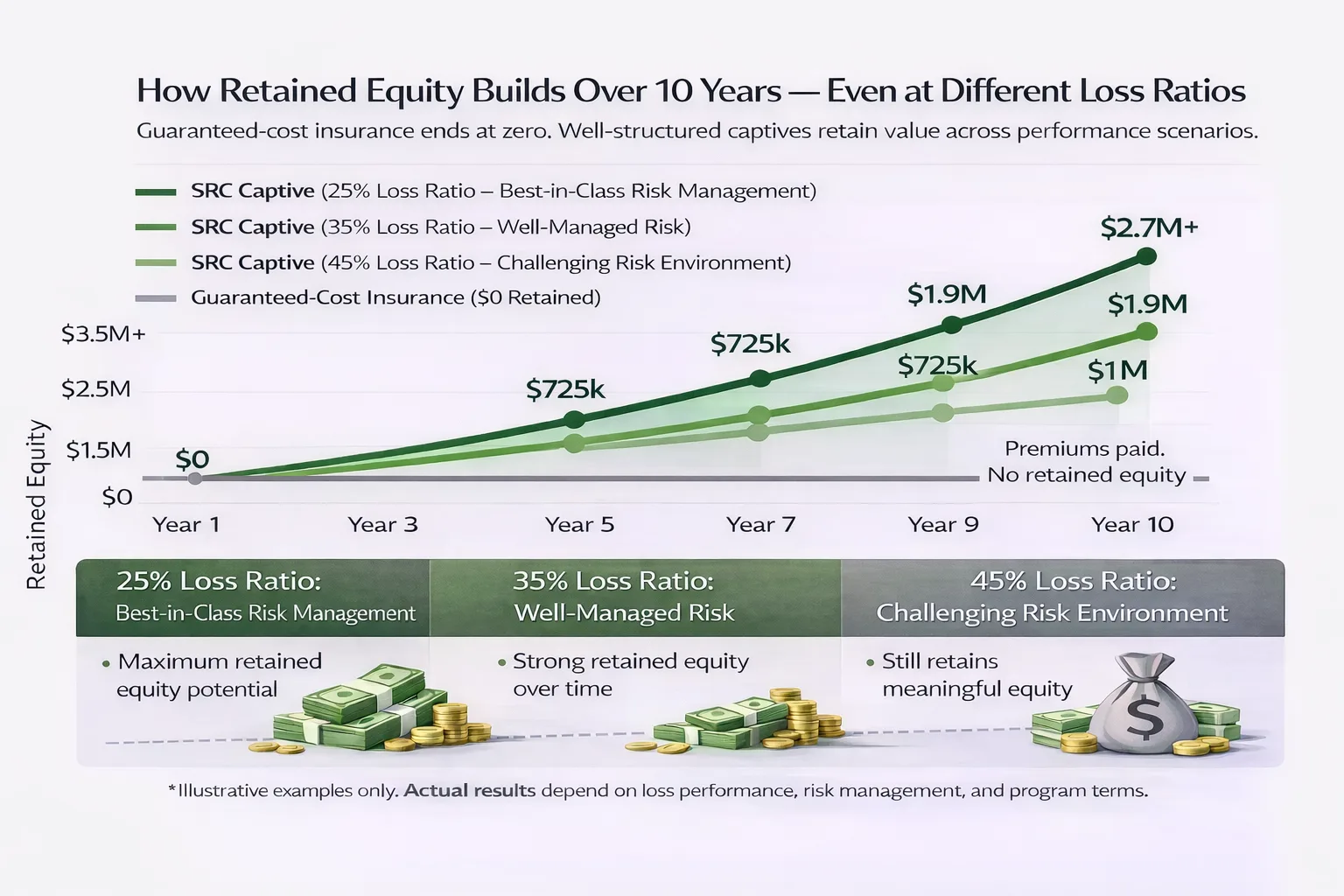

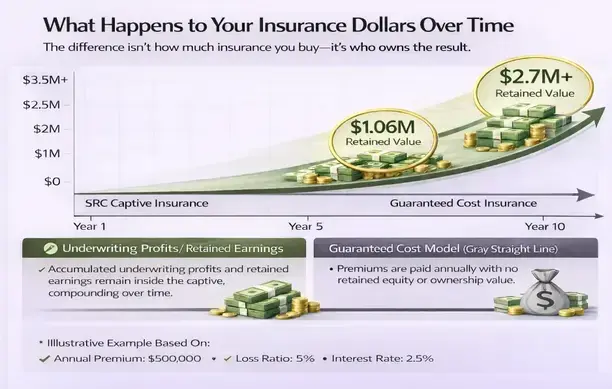

Traditional insurance treats premiums as a fixed expense and transfers underwriting profits to the carrier. SRC restructures insurance into a regulated risk-financing strategy, allowing qualified members to retain underwriting results, invest excess capital, and build enterprise value over time.

What types of risks can be covered through SRC?

SRC is structured around the real operational risks of cannabis businesses, including property-related exposures. Coverage terms are customized within the captive framework and are not constrained by the exclusions and limitations common in standard carrier policies.

Is SRC compliant with insurance regulations?

Yes. SRC operates within established captive insurance frameworks and is structured to meet all applicable regulatory, governance, and reporting standards. Participation is subject to underwriting approval and program guidelines.

Established single-state or multi-state cannabis operators

Established single-state or multi-state cannabis operators Startups

Startups